Q3 2025 Market Update

Quarter in Review: Livin’ on a Prayer

The third quarter closed with markets at or near record highs. U.S. equities rose sharply, with the S&P 500 up 8.1% for the quarter and 14.8% year-to-date. Bonds also gained ground, helped by the Federal Reserve’s renewed rate-cutting cycle. International markets enjoyed another solid quarter, with emerging market equities surging more than 10%. And gold delivered a show-stopping 16% gain, pushing past $3,800 per ounce.

Beneath the cheer, there are caveats. U.S. stock valuations have crept toward levels last seen in the late 1990s. Payroll revisions suggest the labor market is weaker than first advertised. And policy uncertainty, from tariffs to a government shutdown,remains in the mix.

It feels a little like Bon Jovi’s “Livin’ on a Prayer.”The melody is upbeat and hopeful. The chorus is familiar. It’s fun to sing along and enjoy the ride. But the situation is more precarious than it feels on the surface. For investors, this is a time for discipline, diversification, and remembering that record highs don’t change the need for long-term perspective.

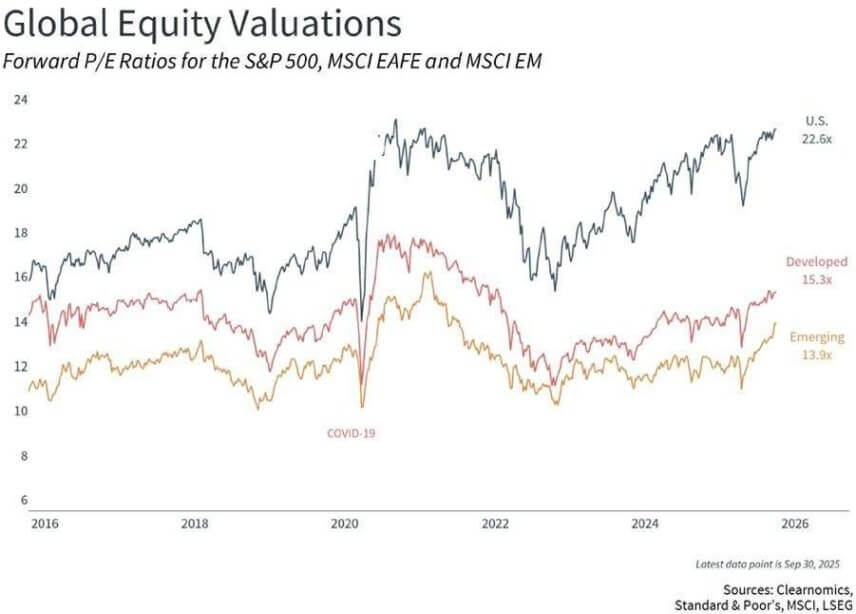

U.S. Equities: Strong Gains, Rich Valuations

The rally broadened in the third quarter. Not only did large caps notch 23 record closes, but small caps finally joined in, with the Russell 2000 up 12.4%. Technology and Communications led the way, while even Utilities and Energy caught a bid. The only sour note came from Consumer Staples, which fell 2.4%.

Growth continues to outrun Value, with the S&P 500 Growth Index nearly doubling the YTD return of its Value counterpart. Much of this can be traced to the“Magnificent 7”stocks, up an astonishing 61% since April. Corporate spending on AI infrastructure is the fuel, though investors are starting to ask questions about the sustainability of AI investments.

Valuations remain the elephant in the room. The Shiller CAPE ratio now stands at 38, far above its long-term average of27 and inching toward dot-com territory. Expensive markets can still rise further, but history says high expectations make future returns harder to earn. Investors may find more attractive entry points in small caps, value stocks, and international equities.

Fixed Income: Fed Part Deux

The Fed eased again in September, the second of the year, cutting rates to a 4.00–4.25% range. The bond market responded appreciatively, as the Bloomberg U.S. Aggregate Bond Index rose 2.0% for the quarter and is up 6.1% for the year.

Treasury yields drifted lower, with the 10-year ending at 4.15%. Credit markets also rallied: investment-grade corporates and high-yield bonds both delivered solid gains. Even munis, left for dead earlier in the year, bounced back with a 2.4% quarterly return.

Importantly, this easing cycle isn’t looking like an emergency rescue mission. Inflation is moderating, growth is slowing but not collapsing, and Fed officials appear to be engineering a “soft normalization.” For income-seeking investors who parked cash in money markets, longer-duration bonds now offer a competitive trade off between yield and risk.

International Markets: Yes,there are markets outside the US

International equities have enjoyed their strongest stretch in years. Emerging markets jumped 10.1% in the quarter and are up more than 21% YTD. Developed markets gained 4.2%, bringing their year-to-date climb to nearly 27%.

Three forces are at play. First, non-U.S. valuations started the year at cheaper levels. Second, the dollar’s near-10% decline has boosted returns for American investors. Third, Chinese stimulus measures have stabilized sentiment in Asia.

For U.S.-based investors, international diversification is more than a slogan. With forward P/E ratios 30% lower than U.S. large caps, these markets offer relative value and different growth cycles.

If equities were a fireworks show, gold was the thunderclap. Up16%in the quarter and 45% YTD, gold broke through both nominal and inflation-adjusted records. Central banks have been big buyers, diversifying away from the dollar at a pace not seen in decades.

FUN FACT:

Gold’s run this year officially broke a 45-year record. Adjusted for inflation, the metal finally eclipsed its 1980 high of $850 per ounce, an era defined by double-digit inflation and disco. Investors who bought a Krugerrand in January 1980 and stashed it in a drawer have finally come out ahead. Whew!

Other commodities were mixed. Energy prices were flat, agricultural goods fell on good harvests, and industrial metals climbed modestly. Real estate investment trusts advanced 2.6% in the quarter, benefiting from lower rates. Hedge funds and digital assets generally rode the same wave as equities, though with less spectacle (and higher fees).

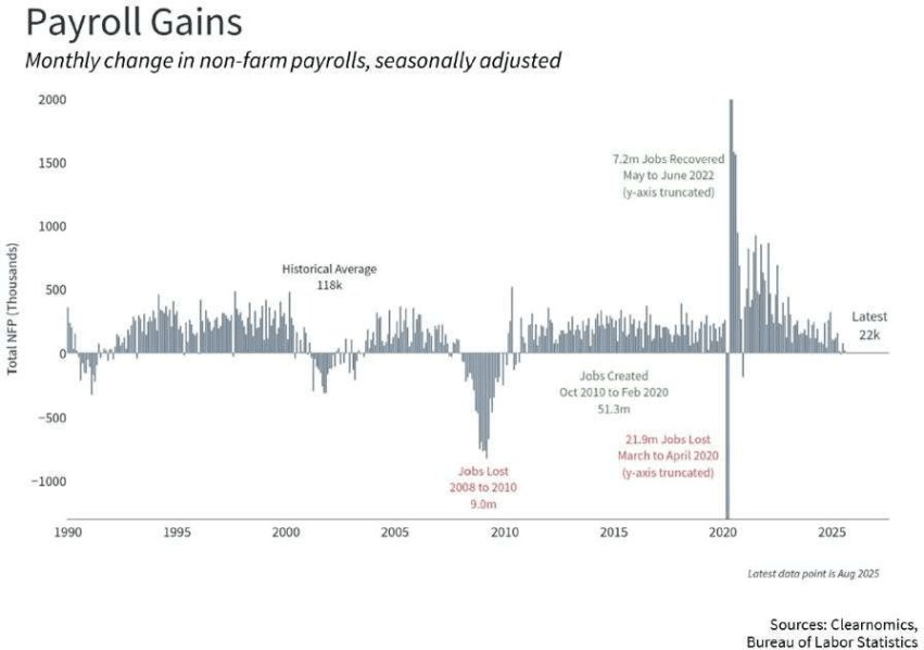

Labor and Volatility: Calm Surface, Uneasy Undercurrent

Volatility measures calmed, with the VIX and the Treasury-focused MOVE Index both below historical averages. But investors shouldn’t mistake quiet seas for a calm climate. Revised payroll data showed nearly one million fewer jobs created than initially reported, the largest downward adjustment in history. That weakness was a key factor in the Fed’s decision to cut rates again.

Closing Perspective: Discipline at the Highs

With markets near records, it’s tempting to believe new paradigms are unfolding. But history says record highs are not signals; they are simply mile markers. The S&P’s strong year-to-date return reflects resilient earnings, easier policy, and enthusiasm for AI. Yet high valuations, payroll weakness, and policy uncertainty suggest investors should proceed with balance, not bravado.

The timeless playbook still applies. Stay diversified across geographies and asset classes. Rebalance to avoid chasing what has already run. Focus on the things within your control – costs, taxes, and behavior – and we’ll make, I swear.

Learn more about MBCEA membership and read additional business management articles.

Sources: Clearnomics, Bureau of Labor Statistics, Federal Reserve, YCharts, S&P Dow Jones Indices, Fortune. Data as of September 30, 2025.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

Securities and investment advisory services offered through Osaic Wealth,Inc. member FINRA/SIPC. Osaic Wealth is separately owned and other entities and/or marketing names, products or services referenced here are independent of Osaic Wealth.